Straight2Bank

Straight2Bank

Finance your life policy premiums for extra liquidity and extend protection to your loved ones

Terms and Conditions apply.

What premium financing is about: Premium financing is an insurance funding arrangement whereby you, as the proposed policy holder, borrow funds from the lender to pay for the premium of the proposed life insurance policy (the “Policy”) and in doing so, you would assign all or part of your rights under the Policy to the lender as collateral.

Here are 2 brief examples* to illustrate how Premium Financing assists to achieve clients’ financial goals in different life stages:

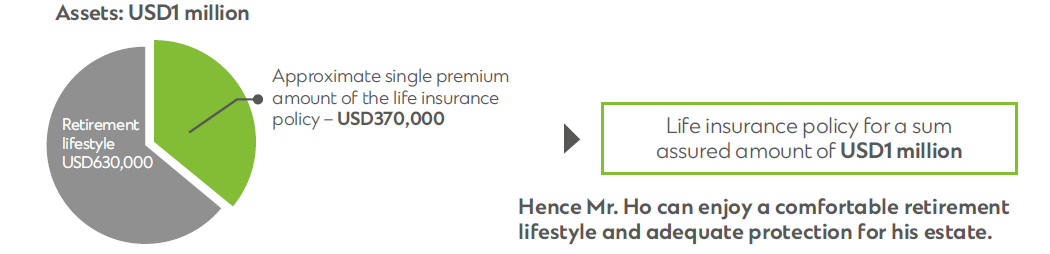

Example 1*

Mr. Ho, age 50 (age of next birthday), non-smoker:

• Has assets totalling USD1 million; and

• Purchases a life insurance policy with a cash payout of USD1 million to his estate.

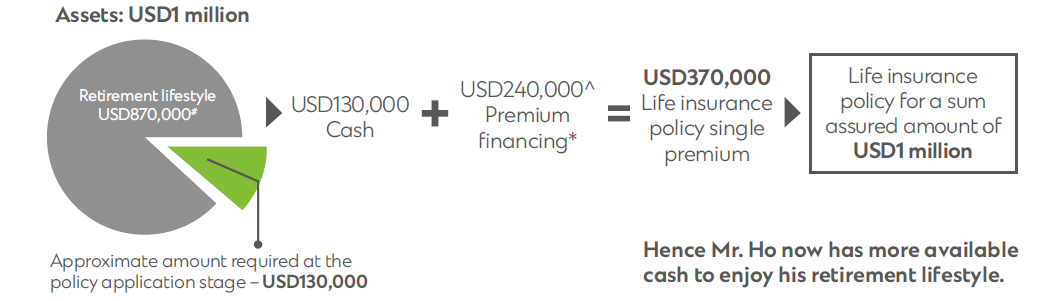

Now Mr. Ho opts to:

• Effect payment of approximately USD130,000 (instead of the entire single premium amount of approximately USD370,000); and

• Obtain premium financing for the approximate balance of USD240,000^

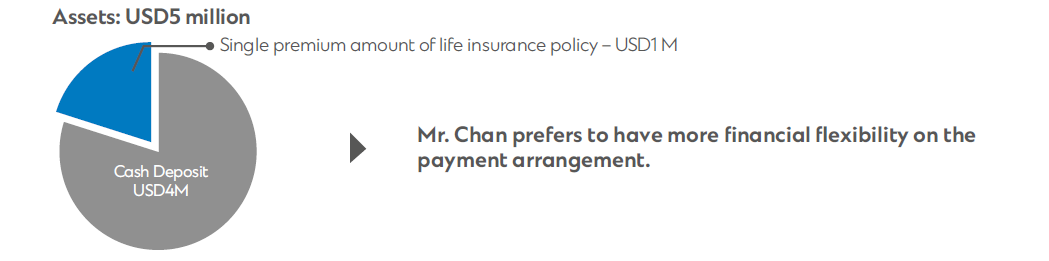

Example 2*

Mr. Chan, age 40 (age of next birthday), non-smoker:

Has assets totalling USD5 million cash deposit;

Decide to purchase a life insurance policy with a single premium of USD1 million to achieve lifelong wealth accumulation and pass down wealth through proper estate planning;

Mr. Chan maintains USD4 million cash deposit as his liquidity

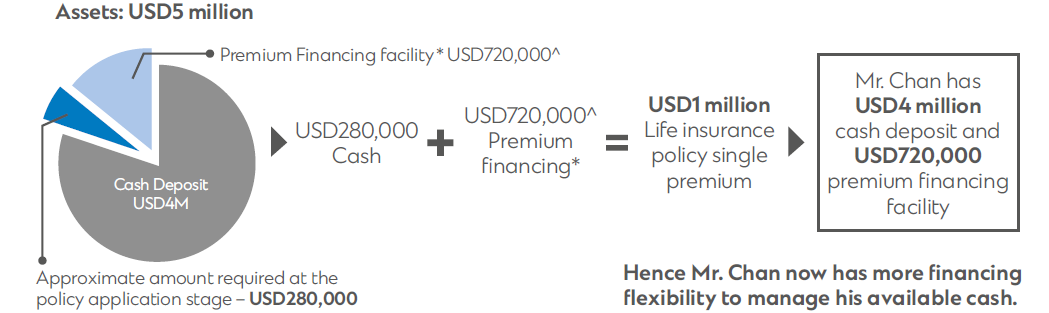

Now Mr. Chan opts to:

Effect payment of approximately up to USD280,000^ (instead of the entire single premium amount of approximately USD1 million); and

Obtain premium financing for the approximate balance of the USD720,000^

Visualize how borrowing impacts the policy net return after interest payments under your expected scenario and risk scenario.

Daily Loan Interest Rate (for reference only)

PAST 30 DAYS | LOAN INTEREST RATE (IN ANNUALISED PERCENTAGE RATE) | |

|---|---|---|

| DATE | HKD | USD |

| 16/10/2025 | 4.76% | 5.79% |

| 15/10/2025 | 4.72% | 5.80% |

| 14/10/2025 | 4.80% | 5.81% |

| 13/10/2025 | 4.74% | 5.83% |

| 10/10/2025 | 4.78% | 5.84% |

| 09/10/2025 | 4.82% | 5.85% |

| 08/10/2025 | 4.85% | 5.87% |

| 06/10/2025 | 4.88% | 5.88% |

| 03/10/2025 | 4.81% | 5.89% |

| 02/10/2025 | 4.79% | 5.89% |

| 30/09/2025 | 4.83% | 5.91% |

| 29/09/2025 | 4.89% | 5.93% |

| 26/09/2025 | 4.90% | 5.94% |

| 25/09/2025 | 4.92% | 5.94% |

| 24/09/2025 | 5.21% | 5.95% |

| 23/09/2025 | 5.21% | 5.95% |

| 22/09/2025 | 4.91% | 5.98% |

| 19/09/2025 | 4.71% | 5.98% |

| 18/09/2025 | 4.66% | 5.98% |

| 17/09/2025 | 4.51% | 5.98% |

| PAST 2ND-12TH MONTH | ||

| 29/08/2025 | 4.59% | 5.95% |

| 31/07/2025 | 2.33% | 5.96% |

| 30/06/2025 | 2.02% | 5.92% |

| 30/05/2025 | 1.88% | 5.93% |

| 30/04/2025 | 5.25% | 5.97% |

| 31/03/2025 | 5.02% | 5.93% |

| 28/02/2025 | 5.26% | 5.95% |

| 31/01/2025 | 5.12% | 5.94% |

| 31/12/2024 | 5.87% | 6.18% |

| 30/11/2024 | 5.60% | 6.32% |

| 31/10/2024 | 5.54% | 6.54% |

Remarks:

| Loan Currency | LOAN INTEREST RATE |

| HKD | 1-Month hibor1 + 1.3% |

| USD | Reference rate2 + 1.3% |

1HIBOR means the Hong Kong Interbank Offered Rate offered on Hong Kong dollar loans in the interbank market.

2Reference rate is a daily interest rate set by the Bank based on respective currency’s benchmark interest rate index. The reference rate may vary daily. For details, please visit the Bank’s branches.

* All figures and examples shown are for illustration purposes only. They are based on a number of assumptions that are not disclosed on this webpage/page and are not guaranteed. Please also refer to the Risk Disclosure and the Important Notes

^ The approval of the premium financing facility (or the “facility”) is subject to the final decision of Standard Chartered. The amount of premium financing is calculated by reference to the Loan-to-value ratio of the Surrender Value or Total Policy Value of the eligible insurance plan as at policy issue date as well as other factors at the absolute discretion of Standard Chartered.

The information on this page is for general information and for reference purposes only. It does not constitute a contract of insurance or Premium Financing or an offer, invitation or recommendation to any person to enter into any contract of insurance or Premium Financing. Customers must not rely on the information in this page alone in entering into any transaction. Specific professional advice is recommended.

Standard Chartered is an insurance agent of Prudential. The life insurance policies are life insurance products underwritten by Prudential Hong Kong Limited (a member of Prudential Plc group) (“Prudential”) and distributed by Standard Chartered Bank (Hong Kong) Limited (“Standard Chartered”). Some of these plans may have a savings element and are not an alternative to ordinary savings or time deposits. Part of the premium pays for the insurance and related costs.

If you are not happy with your policy, you have a right to cancel it within the cooling off period and obtain a refund of any premium and levies paid, less any withdrawals (if applicable), provided that no claim has been made under the policy. A written notice of cancellation signed by you should be received directly by the Prudential’s Office within the cooling off period (that is, within 21 calendar days immediately following either the day of delivery of (1) the policy or (2) the notice (informing the availability of the policy and expiry date of the cooling-off period) to the customer or your nominated representative, whichever is earlier). After the expiration of the cooling off period, if you cancel the policy before the end of the term, the projected total cash value (if applicable) may be less than the total premium you have paid. You should check with Prudential if you have any doubt regarding your cooling-off right.

As the issuer of the life insurance policies, Prudential will be responsible for all protection and claims issues. Prudential is not an associate or subsidiary company of Standard Chartered. Please refer to the policy for full terms and conditions. Standard Chartered does not accept any responsibilities regarding any statements provided by Prudential or any discrepancies or omissions in the contract of insurance nor shall Standard Chartered be held liable in any manner whatsoever in relation to your contract of insurance.

The information of on this page is intended to be distributed in Hong Kong only and shall not be construed as an offer to sell or solicitation to buy or provision of any insurance product outside Hong Kong. Prudential and Standard Chartered do not offer or sell any insurance product in any jurisdictions outside Hong Kong in which such offering or sale of the insurance product is illegal under the laws of such jurisdictions.

Whether to apply for insurance coverage and Premium Financing is your own individual decision. If there is any inconsistency or conflict between the English and the Chinese versions, the English version shall prevail.

To borrow or not to borrow? Borrow only if you can repay!